STABLE, SUSTAINABLE, RISK-FREE

How do reforms form the banking system of Azerbaijan?

Author: Ayaz MUSEIBOV, Financial Analyst, Center for Analysis of Economic Reforms and Communications of the Republic of Azerbaijan

The implementation of the measures stipulated in the “Strategic road maps of the national economy and major sectors of the economy” in Azerbaijan is already showing positive results. The current analysis allows us to state that the banking sector of Azerbaijan has ensured stability and high rates of development.

The preventive measures implemented within the framework of reforms with the aim of eliminating the imbalance between liabilities and assets of banks that maintain high open currency positions during devaluation showed a high effect - banks provided positive dynamics of macro-indicative indicators characterizing the role of banks in the country's economy. Analysis of indicators of the financial stability index of the banking sector, that is, the level of capitalization, liquidity risks, profitability indicators, market risks and asset quality indicates a decrease in risks in this sector. Thus, the sector's assets in 2018 increased by ₼1.5 billion and reached ₼29.5 billion, which is 5.6% growth compared with 2017. Another important indicator is that in 2018, the country's banking sector received a net profit of ₼279 million, while the net losses of the banking sector in 2016 amounted to ₼1.6 billion. Since 2017, there has also been a positive trend in the efficiency indicators of banking assets and capital, ROA and ROE ratios. Along with this, in 2018, the ratio of total assets to non-oil GDP grew by 1.16% and reached 70.94% compared with 2017. There is also a positive development in the number of employees in the banking sector. According to the results of the first quarter of 2019, the number of employees in the banking sector increased by 8.3%, which points to a significant revival of the sector.

The implementation of wide-spectrum redevelopment measures, reducing the proportion of toxic assets in the loan portfolio, strengthening banks' foreign exchange positions, meeting the minimum requirements for liquidity and capitalization contributed to reduction in the proportion of problem assets in the total loan portfolio and improvement in the quality ratio of loan portfolios. Only in 2018, the volume of non-consumptive loans decreased by 1.67% compared with 2017.

Another important point is that, despite the introduction of orthodox expansionist policies in the country's banking sector over the past year, there was a decrease in the share of non-operating assets in the total loan portfolio, which, in turn, indicates that credit decisions are based on the use of advanced risk mitigation tools within control mechanisms.

On the other hand, on February 28, 2019, the President of Azerbaijan signed the Decree “On Additional Measures for addressing Problem Loans to Natural Persons in the Republic of Azerbaijan”, which opened up an entirely new page for the banking sector, creating powerful prerequisites for a significant reduction in the non-performing loan portfolios. The decree will also create conditions for a healthy credit ecosystem, ensuring the influx of real liquid funds in the real sector and a significant improvement in the macroeconomic environment. The significance of the decree for the country's banking sector and its role in solving problem loans were appraised by the influential international rating agencies. Thus, international rating agency Moody’s announced the most positive outlook for the country's banking sector in recent years. The agency, having made changes to the forecasts for Azerbaijan, predicted a reduction in the share of non-performing loans by the end of 2019 from 12% to 10%. It makes it possible to predict with certainty a decline in the ratio of non-performing loans to the planned 8 percent.

Since mid-2017, the trend of reducing volume of deposits in banks due to external economic shocks and the subsequent devaluation of the manat has slowed. According to the results of 2018, the volume of deposits of natural persons in banks reached ₼8.375 billion, which is higher by 12.44% compared to the same period of 2016 and by 10.77% compared to 2017. Over the previous period, there was also recorded a consistent increase in the volume of deposits per capita - by the end of 2018, the volume of deposits per capita amounted to ₼846.16 with an increase of 9.78% compared with 2017.

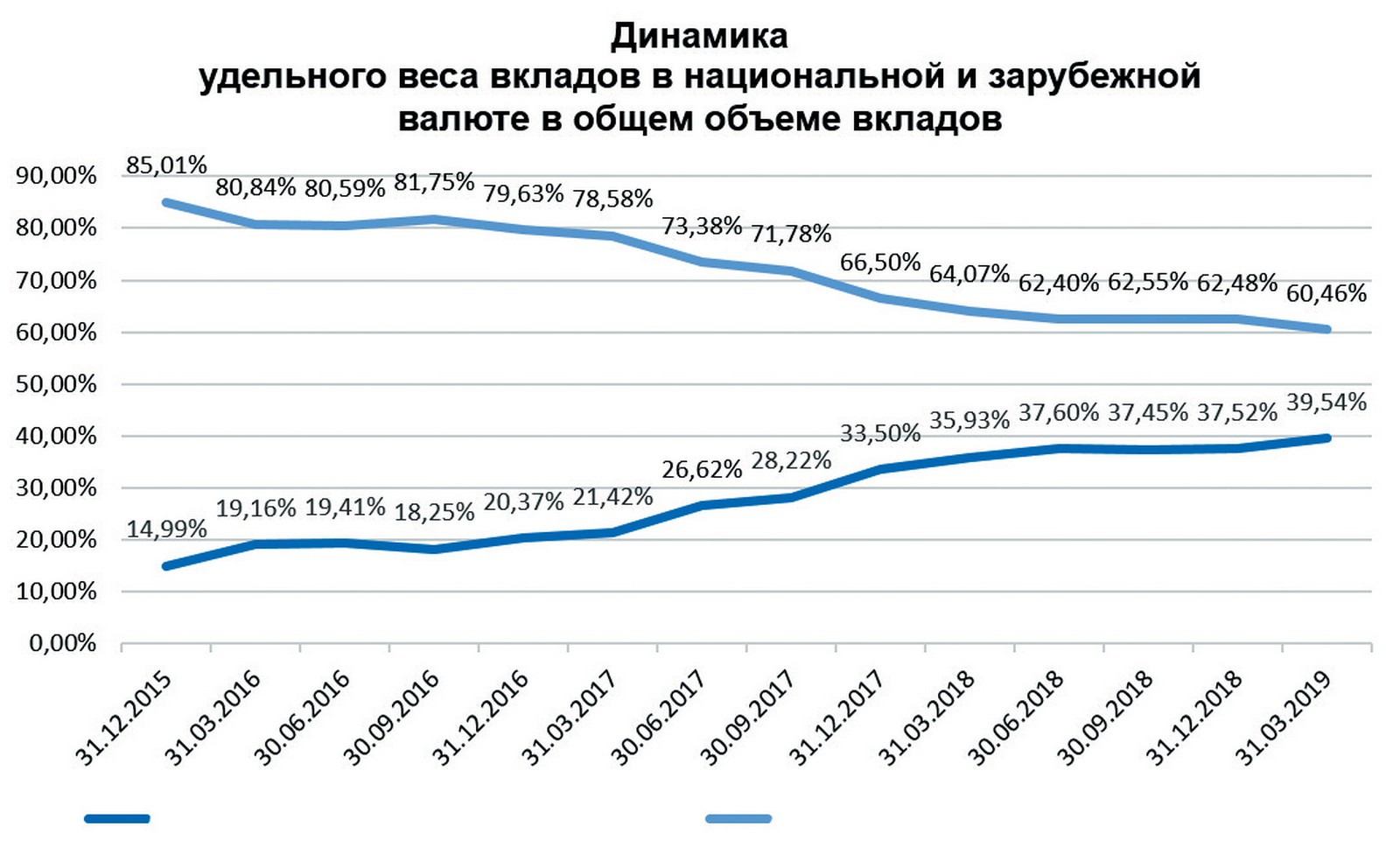

The recorded decrease in the volatility of manat's exchange rate also affected the quality indicators of the structure of deposits. Thus, an indicator of the country's population’s confidence in the banking system and national currency is that, according to the statistics of the last three years, the share of manat in the structure of deposits increased more than 2.5 times compared to foreign currency.

Unhindered access to financial resources and inclusive banking are basic factors of economic development. Numerous studies show that one of the factors that adversely affect the ability to access credit resources is the information deficit. According to the report of the International Monetary Fund for February 2019, one of the greatest difficulties faced by small and medium-sized businesses in the process of access to credit is the minimum amount of collateral and guarantee. According to the world average, the cost of collateral required for a loan is 185% of the loan amount. In particular, this requirement in the South Caucasus region exceeds the world average. Credit organizations operating in the region impose a requirement for collateral in the amount of 245% of the amount of loans issued. The high demand for collateral ultimately reduces the level of credit availability for businesses.

The formation of effective credit reporting systems (CRS) plays a key role in eliminating such problems. It should also be noted the special role of the CRS for the concept of risk management, which is one of the main regulatory trends of the modern period. The numerous studies conducted confirm the presence of a positive correlation between the development of CRS systems and economic development. In order to achieve the level of developed countries in these areas, the Mortgage and Credit Guarantee Fund, the country's first private credit bureau and institutional units for movable property were created as part of the reforms envisaged in the Strategic Road Maps. The development of these systems will provide a wide range of numerous value-added services. The most innovative CRS service is considered to be the assignment of an individual credit rating or scoring behavior, which is a system based on mathematical statistical methods and allows the client to predict the ability to repay a loan based on the current credit history. We add that the credit bureau has already begun to introduce various services in the country - credit histories, aggregate requests, mobile, utility reports and an individual credit rating. Only in the first quarter of 2019, 5.511 people checked their own credit reports, which is indicative of the personal control of credit history data and an organized approach to credit history data by citizens, as well as an indicator of the formation of a completely new borrower culture in the country.

Taking into account the above, it can be said with confidence that the economic reforms carried out in the country will contribute to the formation of a qualitatively new banking sector, the development of the payment and credit infrastructure in the new direction, radically changing the nature of the relationship between debtors and creditors. Thus, as in the best international practices, additional opportunities will be created to provide borrowers with a positive credit history of credit products on more favorable terms. In addition, the reality will be a complete change in the nature of financial relations in the country, as well as the creation of new debt mechanisms and forms of financing. Decisions to issue small consumer loans will not be based on income estimates, but on methods for calculating expenses, and indirectly debts, as provided for in developed financial mechanisms. At the same time, business and the real sector will be financed on the basis of rating models. In particular, credit restrictions (“finance gap”) faced by small and medium-sized businesses in the early stages of development (start-ups) due to limited official information sources, collateral and information asymmetry will be eliminated, and conditions for obtaining credit resources will be created on the principle of "collateral of reputation." At the same time, the ongoing institutional reforms will allow banks to build an effective credit risk management system, which will have a positive impact on saving operating costs, simplifying assessment and underwriting procedures, reducing credit and operating risks, as well as strengthening the financial discipline of borrowers and, ultimately, increasing financial inclusion in the country.

In short, the establishment of a stable banking system in Azerbaijan, adapted to the economic requirements of the post-oil period and functioning on solid foundations and capable of absorbing (minimizing) external shocks, is fast approaching.

RECOMMEND:

293

293