PROTECTING THE CONSUMER

Azerbaijani insurers can issue compensations if DVR images of accidents are available

Author: Nurlana QULIYEVA Baku

The insurance market, being one of the pillars of the financial sector in Azerbaijan, is still significantly different in its development level from the banking sector. Despite steady growth, we cannot say that insurance has become ingrained in ordinary citizens' lives as firmly as banking. Today, both supervisors and market participants are actively trying to eliminate gaps, looking into complaints, carrying out spot checks and promising that insurers become more trustworthy in the near future. In addition, there are proposals to improve the most popular insurance services as of today. All of these issues were the subject of discussion at the 2nd National Forum of Insurance Agents a few days ago.

Guilty without Fault?

It is no secret that insurers in Azerbaijan are most often approached by owners of vehicles. In addition to mandatory insurance, voluntary services of this type are also quite common. However, customers who have placed confidence in insurance agents are not always satisfied in case of an accident: getting an adequate compensation may turn out to be a long, tedious and nerve-racking thing.

Sometimes this happens through the fault of the policy-holders themselves, and here is why. In different parts of Baku and on regional motorways, we all have repeatedly seen cars with ads, sometimes written ungrammatically and by hand, reading as follows: "Car Insurance in few minutes and cheaply". It looks like there is nothing illegal about it: insurance contracts are concluded by insurance agents who are not required to sit in the office: they can easily knock on any door to offer their services. However, not all agents on the market today have the legitimate right to represent an insurance company and, accordingly, to make any transactions on its behalf. This is why "subagents" - persons to whom agents have allegedly transferred their rights - have become common in the market lately.

As it turned out, it is the most common fraud which is certainly punishable by the law. According to Musviq Israfilov, deputy head of the State Insurance Supervision Service, systematic spot checks in the market of insurance agents have revealed cases of insurance contracts concluded by persons who do not represent any insurance companies and have no licence to work as insurance agents. In addition, the agents do not always accurately indicate the necessary information in the contracts which ultimately becomes an obstacle to obtaining insurance compensation or complicates the process. "The latest spot-check of insurance agents was conducted in June and July this year but we will continue such monitoring to detect problems in the market," said M.Israfilov.

Before entering into a contract, it is important for potential customers to inquire if the person representing an insurer has adequate powers, by simply asking them to show their certificate and license.

Mahir Abdullayev, the head of the department of licensing, applications and complaints at the State Insurance Supervision Service of the Ministry of Finance, Azerbaijan has 800 licensed insurance agents today including 52 legal entities and 748 individuals. This indicator shows steady growth dynamics which will remain as the market develops.

M.Abdullayev recalled that amendments to the law "On insurance activity" were adopted in October, some of them dealing with regulation of insurance agents' activity. "According to these amendments, it will be possible to conclude insurance contracts in electronic form. In addition, every three years, agents will have to undergo mandatory certification at the State Insurance Supervision Service", he said. Under the amendments, insurance agents will also have to submit quarterly and annual reports on their activity to the State Insurance Supervision Service.

According to Namiq Xalilov, head of the State Insurance Supervision Service at the Ministry of Finance of Azerbaijan, the problem of individual bad faith insurers is not unique. "It was, is and will be present in all markets, including Azerbaijan. For example, more than 16,000 payments have been made in the current year on compulsory vehicle insurance. At the same time complaints in this segment account for about 1 per cent of this figure. This indicates the level of customer satisfaction," said Xalilov.

According to him, one must also consider other factors. For example, a citizen files a complaint and it turns out during its consideration that the amount paid to the person by the insurance company is legitimate and complies with the contract. However the citizen believes that they should have paid more. "You ask him what's wrong. He replies: I have an outstanding bank loan and I wanted to get more money to repay it. Therefore complaints should be judged not only by their number but also by their true essence," said Xalilov.

Regarding the issue of extremely low amounts of payments by some insurance companies compared to their collected premiums, the state service head explained that the insurers' portfolio pattern also plays a role. "Aviation insurance could be cited by way of example: if there are no accidents, aviation insurers' payments equal zero. While companies whose portfolio is built mainly on the basis of, say, health insurance, the premium to benefit ratio is high" - said Xalilov.

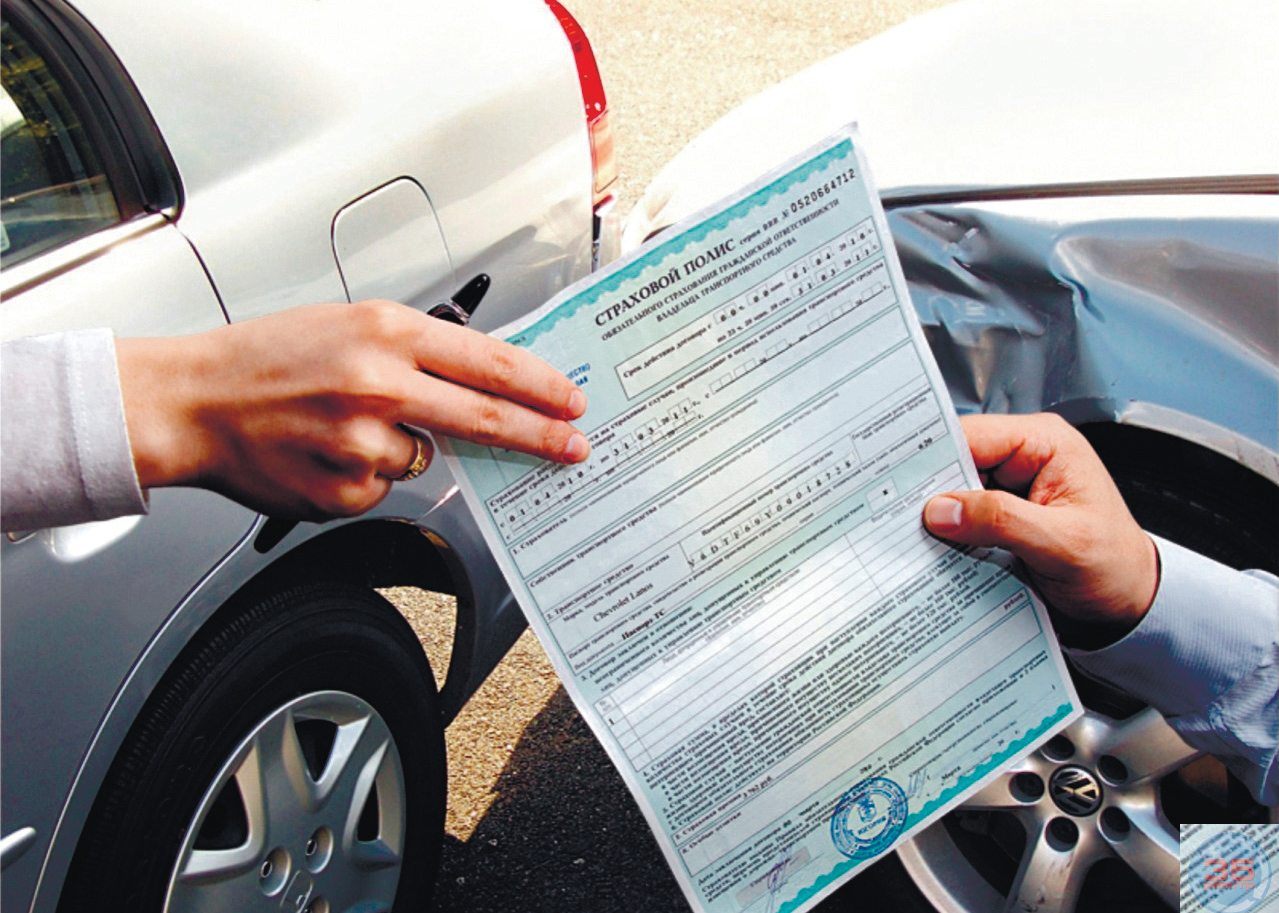

Just one image will do

Meanwhile, both insurance market regulators and participants themselves agree that the number of procedures for obtaining compensation in insurance events are sometimes unnecessarily complicated and need some amendments favourable for consumers.

Thus, according to the regulations currently in effect, insurance companies decide whether to make or refuse to make a payment upon examination of a traffic police report. But since it often takes a long time to receive an accident report, the customers are unhappy with insurers' work. Therefore, the Azerbaijani Insurers Association (ASA) has suggested using recordings from dashboard video recorders (DVR) as a basis for insurance payments in cases of accidents. Such practices would solve several problems. The association believes that such practices will reduce the insurance company's costs arising from the need for insurance experts to visit the accident scene.

"This proposal comes from the ASA and we believe it is right. In addition there is no need to make any changes in the current legislation for the use of video recorders,"- said Xalilov. Insurance companies, he said, may agree among themselves and use DVRs as a basis for insurance payment in case of an accident. Xalilov said that the use of such a system will also speed up insurance payments.

Note that, in January-November 2013, the Compulsory Insurance Bureau (ISB) already paid compensation totalling 49.891 manats to victims of road traffic accidents. According to Nizami Karimov , the head of the ISB department for IT training and support, the office received 25 applications for compensation from victims of road accidents and the families of persons killed in such accidents over the first 11 months of 2013 and 20 of them have already been paid their compensations.

At the same time, according to N.Xalilova, due to changes in legislation, 2014 will see an increase in the volume of insurers' payments under compulsory vehicle insurance as regards damage to life.

According to him, the unprofitability of compulsory vehicle insurance is now at an acceptable level. "At present, the loss ratio for compulsory vehicle insurance is below the critical level of 72 per cent in Azerbaijan. Next year, we also expect that the loss ratio for this type of insurance will be below 70 per cent. Therefore there is no point in talking about revising compulsory vehicle insurance tariffs," he added.

Meanwhile, according to the Compulsory Insurance Bureau, in January-November 2013, compulsory vehicle insurance premiums exceeded 65m manats under more than 856,000 insurance contracts. Compared with the same period last year, this is a 4.22 per cent decline and a 1.4 per cent increase, respectively. The reduction in premiums was caused by changes in the legislation and the use of the bonus-malus system.

N.Karimov said that some 97,700 compulsory vehicle insurance contracts were concluded in 2013 with the use of the bonus-malus system. "The bonus system (with reduced compulsory vehicle insurance premiums) was applied in 96 per cent of the contracts applied. The malus system was used in 4 per cent of the contracts (with insurance rate increased based on the fact that the motor vehicle driver caused road accidents during the previous contract period)," he said.

In short, despite the decline in premiums, insurers are ready to ease the conditions for their customers to receive insurance compensations, being aware how important this is in terms of enhancing confidence in the market in general as well as the population's interest in other types of insurance services.

NOTE

Insurance policies for compulsory vehicle insurance with new rates and terms were offered for sale in Azerbaijan on 16 December 2011.

In particular, the basic rate was fixed at 50 manats for vehicles with engine displacement of up to 1,500 cu.m. Coefficients ranging from 1.5 to 5 are used for engines with bigger engine displacement. Coefficient 5 is applied for vehicles with engine displacement over 5,000 cu.m. i.e. insurance rate is 250 manats.

Coefficient 3 to the basic rate is applied to buses and passenger minibuses with 9-16 seats and coefficient 4 is applied to buses and passenger minibuses with over 16 seats. Coefficients 3 to 5 are applied to lorries depending on their maximum carrying capacity. Coefficient 1 is applied to motorbikes, tractors and other agricultural vehicles.

In addition, the bonus-malus system is used when defining insurance premium of compulsory vehicles insurance.

Under the law on compulsory vehicles insurance, 5,000 manats is paid as insurance money to compensate property damage, 5,000 manats are paid per person as insurance money to compensate health damage and 50,000 manats is a total limit for one insurance event. Thus, the maximum insurance payment under the compulsory vehicles insurance may be as high as 55,000 manats.

RECOMMEND:

848

848