GREECE AT THE CROSS-ROADS

Will Athens be able to get out of being deep in debt and remain in a united Europe?

Author: Fuad HUSEYNALIYEV Baku

To pay or not to pay, that is the question? For the Greeks last Sunday's response to this issue was considerably more important than the conundrum faced by Shakespeare's Hamlet in his monologue "To be or not to be".

Greece, which is the cradle of European civilisation, the source of democracy in the world, has inscribed its name in the contemporary history of the Old World. In this case, it is by no means in a positive way. Among the EU countries and the group of developed countries, for the first time in history Greece has defaulted on its repayments to the International Monetary Fund (IMF). It is precisely this step that is the reason for the referendum, in which the Greeks had to reply to the question whether they were in agreement with the conditions laid down by the international creditors regarding the new loans.

The problems with the Greek economy did not by any means start yesterday and even during the 2008/2009 crisis. According to the report "Oxford Analytica Greece: Austerity package fails to convince", from the moment the Second World War ended, Greece has always been the recipient of assistance from outside. "To begin with, it was the Marshall Plan, then US grants for arms purchases and finally massive cash injections from the EU. All this instilled in Greece a political and economic culture of dependence," the report's authors note.

Greece even entered the Euro-zone in 2001after juggling with the budget deficit and foreign debt figures, since those figures did not correspond to the Maastricht Agreements (the national debt should not be more than 60 per cent of GDP [Gross Domestic Product] and the budget deficit equal to 3 per cent of GDP). Here of course the EU leadership can be reproached for being interested in attracting Athens into the currency union in order to show other would-be member-countries the result of productive reforms. You see, back in 1999 the EU rejected Greece's bid to join the Eurozone. But the Greek reforms just remained on paper.

Although in the early years after the introduction of the euro, Greece's economic indices did go up and inflation fell and the country started to be the recipient of foreign loans at a considerably cheaper rate, the restructuring of the economic model did not take place.

From the point of view of the observance of employees' rights, Greece may be regarded as a socialist paradise. Until recently, 14 wages were paid per year, pensioners could receive a monthly pension of more than 1,400 euros and there were numerous welfare increments; for example, the unmarried daughters of deceased civil servants and military men received pensions. As a result, by mid-2000, according to figures from the Greek newspaper "Kathimerini", the country had become the biggest purchaser in the world of Porsche Cayenne cars per head of the population, more than 50 per cent of Greek infants were born in private clinics where the cost of having a baby was more than 10,000 euros. A considerable part of the workforce was moreover concentrated in the state sector which accounts for as much as 40 per cent of the country's economy.

But the situation relating to tax collection was by no means all that rosy. According to figures from the [Russian] "Kommersant" newspaper, the small businessmen, doctors and lawyers only declared their earnings up to 12,000 euros, which made it possible for them to evade paying tax altogether.

According to the 1967 Constitution, the international merchant shipping was not subjected to taxes on its earnings. You see, Greece has the biggest merchant fleet in the world, and this sphere accounts for up to 7 per cent of GDP. Similar legal loopholes could be found in other sectors too.

As a result, Greece was not able to get back on its feet after the 2008/2009 crisis. Having requested 110bn euros-worth of assistance in 2010, two years later Greece requested another 130bn euros. When it was allocated, as a second package of assistance, a debt of almost 100bn euros was cancelled. The troika of creditors in the form of the International Monetary Fund, the European Commission and the European Central Bank, made the allocation of the loans dependent on stringent budget measures, the restructuring of the economy, the downsizing of the state sector with subsequent mass redundancies and privatisation. Athens was far from keen to implement these measures.

Even after crisis-linked reforms, in the Doing Business rating, Greece was 61st out of 189, the last in the countries embraced by the Office of Economic Statistical Research [OESR]. According to the competitiveness rating of the World Economic Forum, the country ranked 81st out of 144.

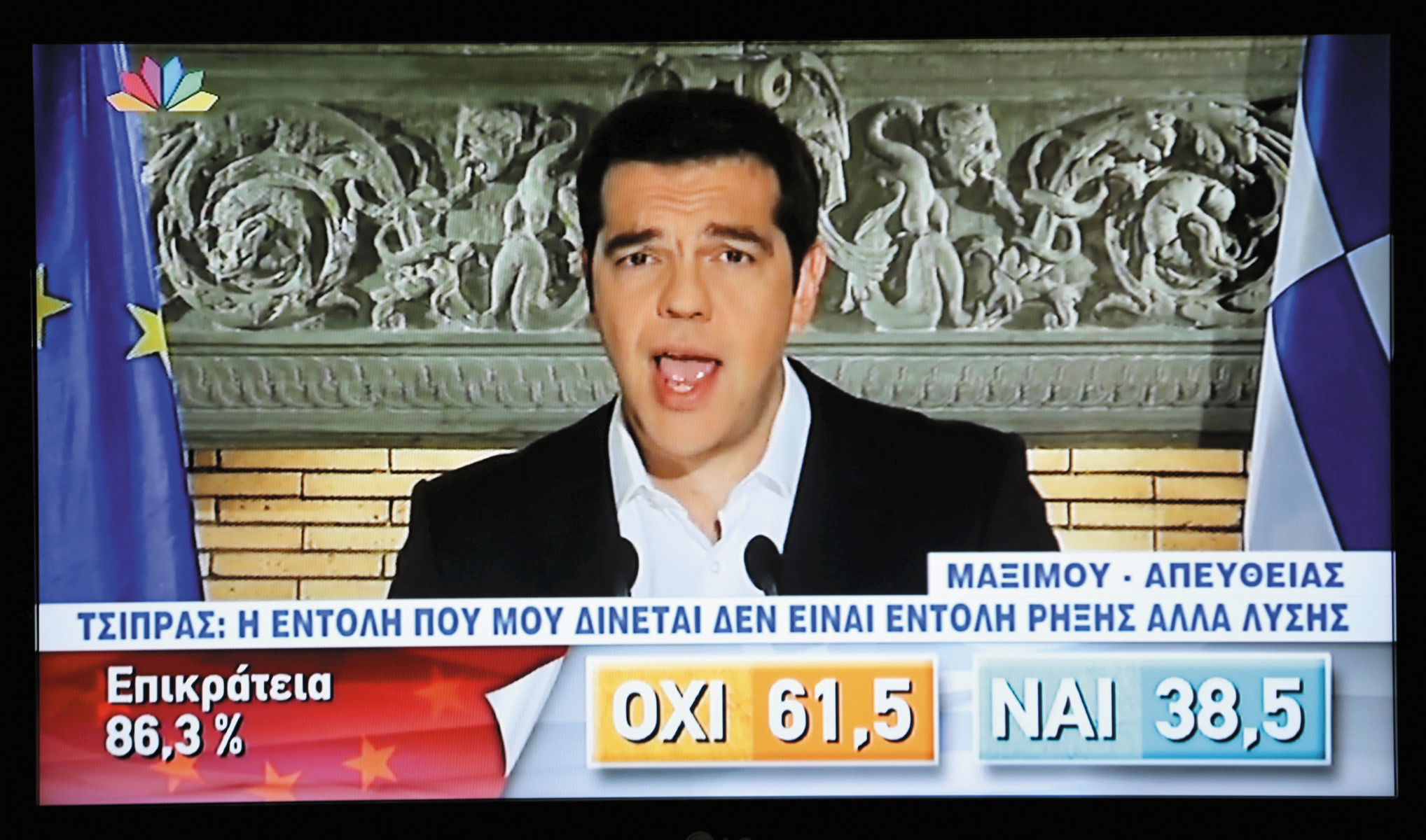

As result, the crisis made its way to 2015 in a planned manner, but in this case, the struggle is promising to be a particularly exacting one. Greece's new left-wing government headed by Prime Minister Alexis Tsipras is demanding that part of the state debt amounting to 320bn euros should be cancelled and that the remaining debt should be restructured and new loans issued. True, in this event, the Greeks are committing themselves to using the new loans solely to pay off the old debt and not for financing the budget deficit, as had been the case up until now.

Incidentally, one of Athens' main creditors, the IMF, has admitted that, unless part of the debt is cancelled, Greece will not survive. Even after that, moreover, Greece is demanding up to 60bn euros in assistance, of which 50bn is needed over the next three years. In its report, the IMF has admitted that, in implementing the former aid programmes, such a steep decline in the Greek economy leading to unimaginable unemployment (more than 25 per cent) had not been forecast.

As a result, Tsipras proposed that the creditors agree to a referendum, in which something like 60 per cent of the population has supported the government's intention to reject the harsh economic measures. They were not the least bit troubled by the closure of the banks for the whole of last week and the threat of leaving the Eurozone and even the EU. Following the outcome of the referendum, Tsipras has stated his intention to come to an agreement with the creditors in the next few days. His haste is quite understandable, since the country has hardly any money left and there is no longer anything to pay even the pensioners with this week.

But it remains a big question whether the European Union will be more inclined to talk. Even before the referendum, the whole EU elite threatened nightmarish consequences resulting from the rejection of the agreement with the creditors. Greece's exit from the Eurozone [Grexit] and then from the EU in general is regarded as the main threat. Moreover, Greece is threatened by a humanitarian catastrophe, since the country does not even have money to purchase fuel, foodstuffs and medicines.

But in Greece itself there is no intention of rejecting the euro. Finance Minister Yanis Varoufakis has stated that the country no longer has even a printing press to produce its own currency, the drachma. Varoufakis has incidentally already tendered his resignation, since "some members of the Eurozone regard his presence at the finance ministers' sittings as undesirable", his statement says.

So, a kind of stale-mate situation is being created.

For their part, the Greeks are threatening to appeal to judicial bodies if the country is forcibly ousted from a united Europe, since no judicial mechanism exists for a country to exit the Eurozone.

Greece is evidently calculating on a repeat of the 2012 scenario when fresh aid was apportioned and part of the debts were cancelled. But the situation is somewhat different now. At that time, Europe not only rescued Greece, but its own united economy as a whole, which had only just got back on its feet after the long-drawn-out crisis. At that time, moreover, there were several states in the risk zone, namely Portugal, Spain, Iceland, Cyprus and even Italy. A crash in any European Union economy might have provoked a chain reaction with catastrophic consequences for the whole world economy.

At the present time, the EU economy and the Eurozone have become stronger to a considerable extent, and the overwhelming majority of experts are not predicting that any kind of global shocks would ensue from Greece's exit from the Eurozone. On the other hand, a concession to Greece may become a headache for the EU on the whole, since there may be other states that wish to copy the "Greek experiment".

After the referendum JPMorgan and Barclays analysts regard Greece's exit from the Eurozone as the basic scenario. This decision may cause a drop in the euro conversion rate, which is at the moment on a minimum level approaching parity with the dollar.

In Europe they calculated on Tsipras's cabinet resigning, as he had stated it would on the threshold of the referendum, in the event of the population supporting the agreement with the creditors. In that it event, it would have been possible to foist their conditions on the new government, but this scenario will have to be forgotten now.

If we analyse the situation in the world, then, except for the troika of creditors, no other rescuers for Greece are particularly in evidence. In spite of Tsipras kowtowing to Russia, it is hardly likely that Moscow is in a position to help Greece in a period when Russia itself is having sanctions imposed upon it by the West. And this show of deference to Russia did not move on from word to deed. Greece has approved the extension, adopted in January and June 2015,of sanctions against Russia, although its vote alone could not change the situation since this type of decision needs the consent of all the EU members.

Naturally, Greece can be reproached ad infinitum for living beyond her means, but it should not be forgotten that the aid programme proposed by the financial institutions, among them especially prominent is the IMF, can often lead to negative results as well. For some of the IMF's main conditions in allocating loans are increasing the charges for communal services, the privatisation of state property, operating a deficit-free budget and other methods of administering the economy by getting the market on track.

It is programmes just like those that the IMF implemented in Azerbaijan as well in the mid-1990s. In total, the country managed to attract approximately 580m dollars from the IMF by carrying out a number of reforms to make the change from a planned to a market economy. But, when exacting demands were made that gas and electricity tariffs should be raised, and also major state assets privatised, the country's leadership preferred to turn down the new loans, after concentrating solely on the Fund's assistance in the form of technical recommendations. The current state of Azerbaijan's economy shows that the decision taken in 2005 was the correct one. Since then Azerbaijan has boasted high rates of GDP growth, having managed to completely repay all the IMF's loans at the same time.

The development of the situation in Greece is of particular interest to Azerbaijan, since it is precisely Ancient Greece that is the starting point for the Trans-Adriatic gas pipeline (TAP), which is to be called upon to transport Azerbaijani gas to Europe. The squabbling in Athens may in theory have an effect on the rate of implementation of this project. Although there is still time, since the gas supplies are not due to start until 2020.

SOCAR's [State Oil Company of the Republic of Azerbaijan] deal to purchase the DESFA gas distribution network from the Greek operator is evoking great concern. Back in 2013 Azerbaijan won the tender to privatise 66 per cent of DESFA and signed an agreement on purchasing its assets for 400m euros, having paid in advance. But, a little later on, the European Commission intervened in a desire to check the impact of the deal on competition. The European Commission's check is to be completed before the end of 2015.

As this investigation was going on, Tsipras's government put a fly in the ointment. Greece's Energy Minister Panagiotis Lafazanis noted that the government is only interested in selling 49 per cent of DESFA. At SOCAR they are not prepared to entertain a variant whereby their share is reduced. As the company's director Rovnaq Abdullayev stated to Regionplus, SOCAR won the tender for the sale of 66 per cent of the shares and not 49 per cent.

"The payment in advance has already been made and a bank guarantee provided. From the Greek point of view, there are no problems regarding this issue. The problem is the European Union. We are currently resolving the issue of completing the deal with the EU's anti-monopoly bodies," R. Abdullayev noted. If Greece should continue to insist on reducing the share in DESFA already sold, that can become a topic to be dealt with at absolutely new talks involving other conditions.

For the moment attention is focussed on whether Greece will be able to get out of debt and remain in a united Europe. The final in this game remains unpredictable, in spite of the many forecasts.

RECOMMEND:

793

793