'GAMES' OF THE 21st CENTURY

Struggle for Rare Earth Metals: Geopolitical Vector of the Century

Author: Irina KHALTURINA

The extraction of rare earth metals (REM) has recently become a key geopolitical issue. The competition for access to these resources is intensifying to the extent that it is being referred to as the 'Great Game of the 21st century'.

The implications of this are significant, as these metals are essential components in the production of numerous high-tech goods, including electronics (computers, smartphones, etc.), solar panels, wind turbines, electric vehicles, medical equipment, and are indispensable in the defense industry and aerospace sector. The unique properties of REM allow for enhanced efficiency and durability, as well as reduced size and weight of products. Given the primary demand for REM in the IT industry and military-industrial complex, the conversation essentially revolves around national security.

In this context, it is notable that the Trump administration has prioritised expanding the extraction and processing of REM as a cornerstone of its policy aimed at 'making America great again'. However, the REM market is almost entirely controlled by China, which accounts for 60% of global extraction and nearly 85-90% of global processing and supply. According to the latest data from the US Geological Survey, China produced 270,000 tonnes of rare earth metals in 2024, doubling its production over five years, while the US produced 45,000 tonnes, a significant gap. The current distribution is as follows: after China, Brazil ranks second in REM reserves, followed by India, Australia, Russia, Vietnam, the US, Greenland, and Tanzania. In terms of REM production, China once again leads the field, followed by the US, Myanmar (which borders China and effectively operates for it), Australia, Thailand (which also effectively operates for China), India, Russia, and Vietnam.

Expert reviews indicate that China began to dominate the global rare earth metals sector in the 1980s. While the situation did not appear as critical a couple of decades ago, Washington has now realised it is increasingly falling into a dangerous dependency on its main competitor on the world stage. The ongoing sanctions war between the two countries has highlighted the leverage China holds, as any increase in tariffs on Chinese goods could be met with restrictions on the export of crucial metals. It is noteworthy that China's President Xi Jinping has referred to REM as 'an important strategic resource'. Notably, China controls its own deposits and also imports from Africa, Central Asia, South America, primarily from neighbouring Myanmar and Thailand. It is highly unlikely that other countries, including the US, will be able to match China's position in the field of REM.

It is important to understand that most REM are not rare in the literal sense, but rather infrequently occur in concentrated quantities sufficient to make their extraction and processing profitable.

The Rare Earth Paradox

The extraction and processing of REM necessitates the use of complex and costly technologies. This is a key factor in explaining why the US has fallen behind China in this field. This is evidenced by the divergent opinions on the relative profitability of the much-discussed US-Ukraine deal regarding REM.

While not all REM are extracted in China, a significant portion is processed there. In contrast, there are only a few plants outside China capable of producing rare earth element oxides on an industrial scale. Historically, the complexity of REM processing has deterred engagement, due to the high cost, labour intensity and environmental impact. Consequently, the decision by China to assume this responsibility was met with widespread approval. Consequently, while comparable enterprises were closing in the US, Beijing initiated a substantial development of extraction, separation, and processing technologies for REM. Consequently, over time, it became increasingly profitable for many companies to send ore for processing to China. This creates a paradox, as the industry, which has a relatively poor environmental record, is now vital to reducing the impacts of climate change. This dynamic is a key factor in explaining the reluctance of Donald Trump to embrace 'green' agendas.

Meanwhile, Beijing has gone even further, not only learning to efficiently extract and process REM, but also using them. While in 2004, China utilised less than half of its produced rare earth metals, it now manufactures high-tech end products that are in high demand and widely trusted worldwide.

Furthermore, specialists note that China maintains REM prices at levels favourable to it to complicate competition from other countries. The intricate interplay between technological progress, environmental concerns, and globalisation processes has resulted in a geopolitical situation that is becoming increasingly evident.

The term 'rare' should not mislead. While REM are abundant in the Earth's crust, only a few can extract or process them effectively, especially when extraction needs to occur in challenging climatic conditions, as is the case in Greenland.

Partner or Enemy?

Russia is a notable example of a country with substantial reserves of REM, with a significant portion located in the Arctic zone, the Far East, and the Irkutsk region. Moscow has the capacity to manage the entire cycle. Recent news indicates that this is in line with its plans to establish a complete line for extraction and processing up to the production of finished high-tech products to meet domestic needs. In February, Russian President Vladimir Putin made a statement to this effect. However, he also made another statement that provoked significant criticism within the country, namely that Russia might invite foreign partners, including the US, for joint work on rare earth metals. It is evident that for Moscow to make progress, it needs relief from sanctions, along with technology and investments. This support is likely to come from either China or the US.

The US is unlikely to accept China's effective monopoly. The US has both promising deposits (in California, Alaska, Wyoming, Georgia, and Texas) and production capabilities, while actively exploring external opportunities as well. Consequently, it is reasonable to hypothesise on the geopolitical dynamics of REM, both in terms of potential future conflicts and those that are already underway: South America (Brazil—the so-called 'Lithium Triangle' consisting of Argentina, Bolivia, and Chile), Central Asia, Afghanistan, Mongolia, India, African nations, and certainly Ukraine.

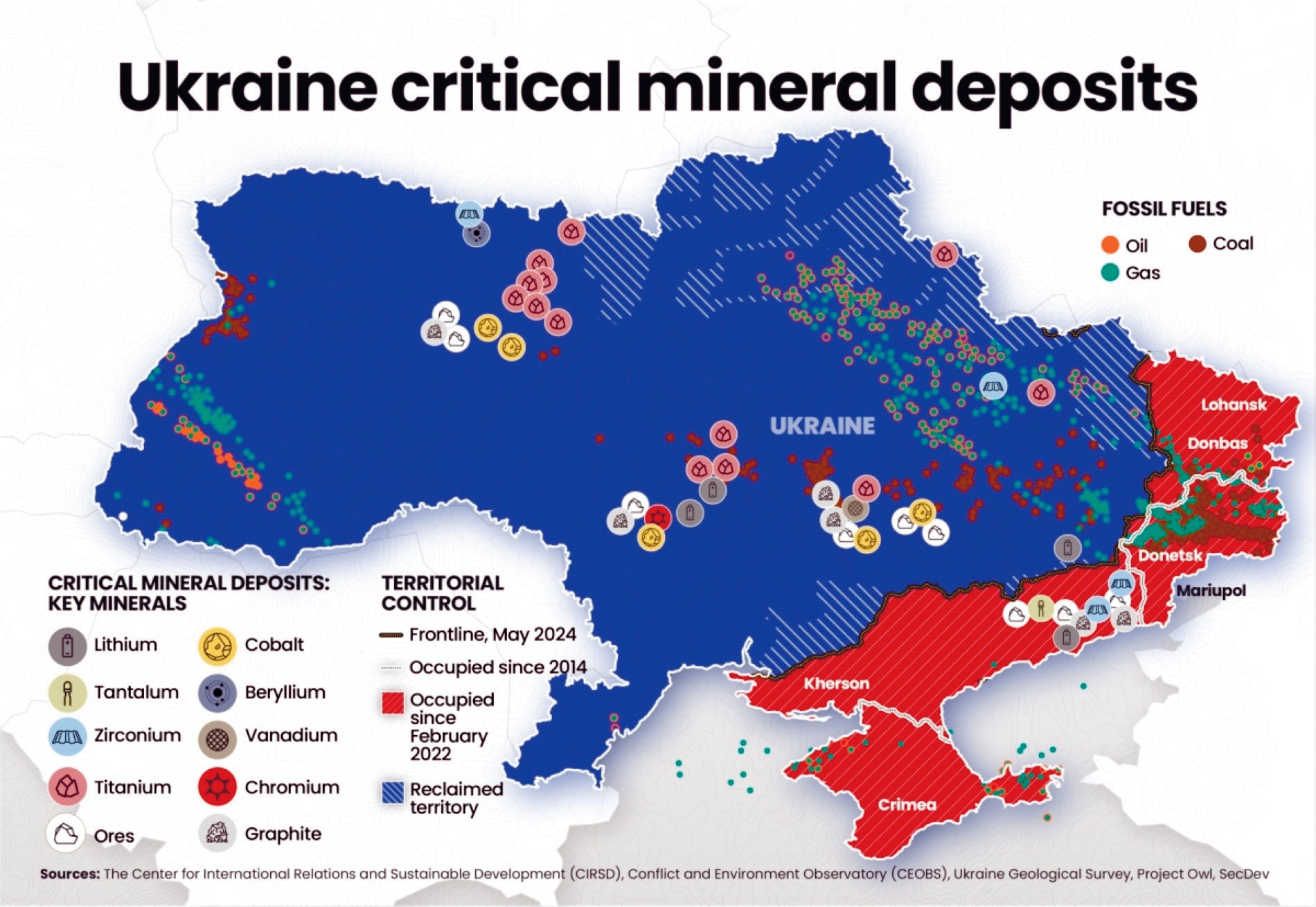

The topic of REM has become closely intertwined with the conflict in Ukraine. Firstly, the war has demonstrated that modern warfare cannot proceed without employing AI, drones, new materials, robots etc. Secondly, President Donald Trump openly expressed the US's interest in acquiring rare earth metals from Ukraine. According to the new US administration, a deal with Kiev concerning REM extraction could serve as a viable means to recoup funds previously spent on military aid to Kiev. However, the most significant aspect for the US is to take steps towards dismantling China's monopoly on REM. According to estimates from Ukraine itself, around 5% of global critical raw materials reside within its territory—including millions of tonnes of graphite reserves, one-third of European lithium deposits and 7% of European titanium supplies. The total value of unexploited reserves is estimated to reach $220 billion. However, Ukraine does not currently rank among the top ten holders of REM. Some experts argue that Kiev's forecasts regarding its reserves are overly optimistic, since there are not many ores there which could be mined profitably. Furthermore, it should be noted that certain strategic resources are currently under Russian control. Even under the most favourable conditions, it remains uncertain how long geological exploration will take and how much funding will be needed to create necessary capacities and infrastructure, especially since some deposits lie beneath infrastructure objects such as roads, populated areas and power lines.

These challenges are not unique to Ukraine, as similar issues are observed in other countries and regions where REM are believed to exist. Internal instability and armed conflicts (Ukraine, Afghanistan, African nations like South Africa, Rwanda, Congo and Burundi) may also obstruct extraction and processing efforts. Additional challenges may arise due to challenging climatic conditions or difficulties in concealing environmental damage (Canada, Russia, Greenland, Svalbard, Alaska, Sweden, Norway and Japan's economic zone in the Pacific Ocean). It is important to note that ores from which REM are extracted often contain thorium and uranium, which are radioactive materials that can contaminate groundwater and streams. Furthermore, large volumes of water and energy are required for extraction and processing. The harm inflicted on the environment is already evident in southern China's mountains and northern Myanmar. The largest rare earth deposit in China, located in Inner Mongolia's Baotou, is among the most polluted places on Earth. Consequently, those countries that can develop an environmentally friendly and economically efficient process for extracting and refining REM stand a better chance of advancing their position.

Finally, logistics are a critical aspect of the 'battle for rare earths', particularly for regions disconnected from global maritime trade routes (Central Asia, Mongolia, Afghanistan). It is clear that diversifying not only extraction locations but also supply chains is essential. This may indeed explain why geopolitical struggles have intensified over new trade routes recently. Just as discoveries of fossil fuel reserves shaped the last century, so too does the race for REM shape the 21st century. The technological development of the rare earth metal sector is critical for the competitiveness of any country, and this issue will become increasingly significant on the geopolitical world stage.

RECOMMEND:

241

241