A GLOBAL PROBLEM

The war in the Middle East can trigger the most severe recession in the global economy

Author: Nurlana GULIYEVA

Regardless of the outcome of the war in the Middle East, it was evident from the outset that its economic consequences would be long-term and global in nature. The question of closing the Strait of Hormuz – a key route for global energy trade – has prompted both international financial institutions and analysts to issue forecasts and warnings of a panicky nature.

Is the situation as critical as it is being made out to be? Which sectors of the global economy are being hit hardest by the Middle East crisis, and who will suffer the most? The answers to these questions are of concern not only to economists.

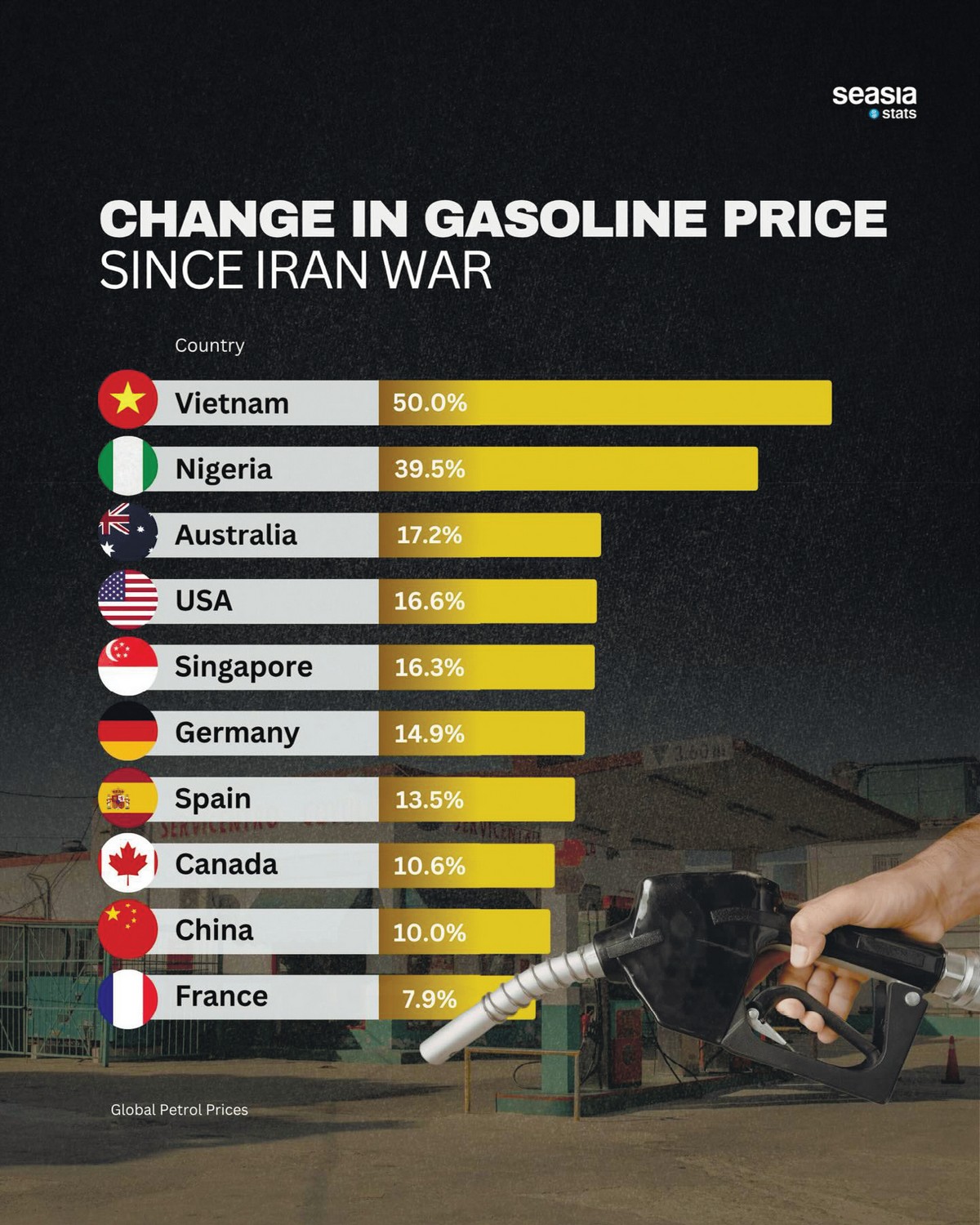

Consequences for the energy market

Firstly, it is important to consider the significance of the Strait of Hormuz to the global economy and the reasons why the situation surrounding it is a cause for concern. This narrow waterway connects the Persian Gulf with international markets. Approximately 20% of global trade in oil and liquefied natural gas passes through this region.

The strait also transports many components essential for sectors such as the aerospace and automotive industries, the chemical industry, and the production of fertilisers, microchips and even MRI machines. Experts predict an acceleration in inflation rates across Europe, the US and Asia. It appears that this is one of the least problematic options.

As highlighted in a recent study by the International Monetary Fund (IMF), the surge in energy prices has already had a substantial impact on importers in Asia and Europe, comparable to the repercussions of the 2021–2022 gas crisis. At the same time, analysts have stated that the issue is not limited to rising prices. In several regions, primarily in Africa and Asia, difficulties are already being reported with physical access to supplies, even at higher prices.

In this situation, the European market is once again facing risks that seemed to have been consigned to the past following the energy crisis of recent years. The IMF emphasises that countries such as Italy and the UK are particularly vulnerable due to their reliance on gas-fired power stations, whilst France and Spain are relatively protected thanks to their greater capacity in nuclear and renewable energy.

The negative impact is not limited to importers. Even the Gulf states, which have traditionally benefited from high oil prices, may experience a slowdown in economic growth. Rising insurance costs, investment risks and disruptions to established logistics routes are creating new constraints on capital inflows and the implementation of infrastructure projects.

The scale of the current crisis is significantly larger than that of classic energy shocks. As Fatih Birol, head of the International Energy Agency (IEA), stated, the world is currently facing an unprecedented threat to energy security: 'We have never seen anything like this before. During the 1970s, there were two significant oil crises, in 1973 and 1979. At that time, the total loss of global oil production was 10 million barrels per day. In the current crisis in the Middle East, however, daily losses are greater than during the two crises of the 1970s combined."

It is estimated that daily losses currently stand at 11 million barrels. In comparison, alternative routes are only able to provide approximately 4 million barrels per day. Concurrently, there has been a decline in gas transport, exerting pressure not only on the energy sector but also on industry as a whole. "In the context of the ongoing war between Russia and Ukraine, natural gas supplies have decreased by 75 billion cubic metres. At present, due to a decrease in exports from Qatar and the UAE, losses have reached 110 billion cubic metres. Domestic gas supplies in these countries have fallen by a further 30 billion cubic metres," noted Birol.

Stabilisation efforts for the market are already in progress, but their impact has been restricted thus far to a limited and short-term basis. Following the IEA's initiative on 11 March, 400 million barrels of strategic oil reserves were released, leading to a temporary decrease in oil prices of $18. However, the resumption of bombings resulted in a subsequent rise in prices. Birol also stated that the agency is prepared to continue utilising its available reserves.

All-sector shock wave

The impact of the Middle East conflict is already extending far beyond the energy sector, gradually transforming into a systemic crisis in global transport chains. A significant proportion of not only oil and gas, but also raw materials for the petrochemical industry and fertilisers, pass through the Strait of Hormuz, which directly affects the agricultural sector.

High energy prices have a number of ramifications for the economy. For households, this means a decline in purchasing power; for businesses, it means rising transport and production costs and, consequently, an impact on profitability. Concurrently, financial markets are experiencing mounting pressure. Geopolitical uncertainty has historically led to increased demand for safe-haven assets, resulting in a strengthening of the US dollar and a tightening of global financial conditions. This has in turn raised borrowing costs and increased risks for emerging economies.

In addition, as Jorge Moreira da Silva, head of the UN Office for Project Services, points out, the conflict is already causing serious disruptions to global trade: "The closure of airspace, sea routes and key crossings is hindering the delivery of vital goods, including medicines."

The agricultural sector is proving to be the most vulnerable. According to Abdolreza Abbassian, a former representative of the UN Food and Agriculture Organisation, even a short-term continuation of the conflict could lead to unprecedented consequences: "If the war continues for another month or more, we are facing an emergency of immense proportions, one that is unlike any we have previously experienced."

A significant portion of the trade in nitrogen fertilisers has already been halted or is under threat. Furthermore, the conflict has coincided with the start of the sowing season in the Northern Hemisphere, which amplifies the potential impact on global agriculture.

Experts stress that the consequences could become apparent in the very near future. According to analysts, the potential loss of fertilisers could have significant consequences for global agriculture, potentially resulting in rising food prices. Given that the cost of gas accounts for up to 80% of the cost of fertilisers, the energy crisis automatically exacerbates shortages and price pressures in the agricultural sector.

The second area affected by the crisis is industry; persistently high fuel prices could have a negative impact on energy-intensive sectors such as the chemical industry, metallurgy, and the production of fertilisers and building materials.

It should be noted that physical disruptions to logistics are an additional factor. Restrictions on shipping in the Strait of Hormuz have already led to longer routes and higher transport costs. As a result, carriers are forced to reroute ships around the African continent, which increases delivery times and adds thousands of kilometres to routes.

A similar situation is unfolding in the metals market. Gulf countries account for approximately 9% of global aluminium production, and any disruption to exports has already resulted in price increases that have reached multi-year highs. Producers are currently unable to ship their products, which is having a further negative effect on the global market.

Concurrently, the petrochemical sector is experiencing similar challenges. According to analysts' estimates, the Middle East accounts for up to 15% of global polyethylene production. Any disruptions at ports and logistics hubs have a direct impact on supplies to the plastics industry and related sectors.

Taken together, these factors are creating a widespread inflationary impulse. As noted in a report by the European Bank for Reconstruction and Development, "if trade to and from the Gulf states continues to be disrupted, temporary shortages and upward price pressures on the production of aluminium, sulphur, helium (for semiconductors), petrochemicals, plastics and other goods may intensify in the short term, spreading through supply chains and amplifying the global inflationary impact".

Asymmetric impact

In such circumstances, the key risk to the global economy lies not only in the rise in prices themselves, but also in their duration. The protracted nature of the crisis could trigger a classic inflationary scenario, followed by a slowdown in economic growth and an increase in the debt burden, which inevitably returns the economy to the challenges it faced during the major energy shocks of the past.

As the IMF study emphasises, the shocks are global but asymmetric. Energy importers are more vulnerable than exporters, with poorer countries being more exposed than richer ones, and those with fewer reserves being more vulnerable than those with more.

In essence, this is a matter of risk distribution within the economy. The most vulnerable countries are precisely those least able to adapt to external shocks. At the same time, according to the Fund's experts, 'the world is facing yet another shock', which is superimposed on the still-ongoing process of recovery from previous crises.

The potential consequences for countries directly involved in the Middle East conflict are a further cause for concern. According to IMF experts, the damage to infrastructure and industry could be long-term, with implications for economic growth in the years ahead. In the short term, this will inevitably result in a slowdown in business activity and increased pressure on public finances.

It is clear that, when viewed in totality, the current crisis must no longer be considered as a mere temporary disruption or a localised energy shock. The speed at which key global trade hubs can be stabilised will determine whether this crisis remains a passing episode or becomes a new starting point for the global economy.

RECOMMEND:

118

118